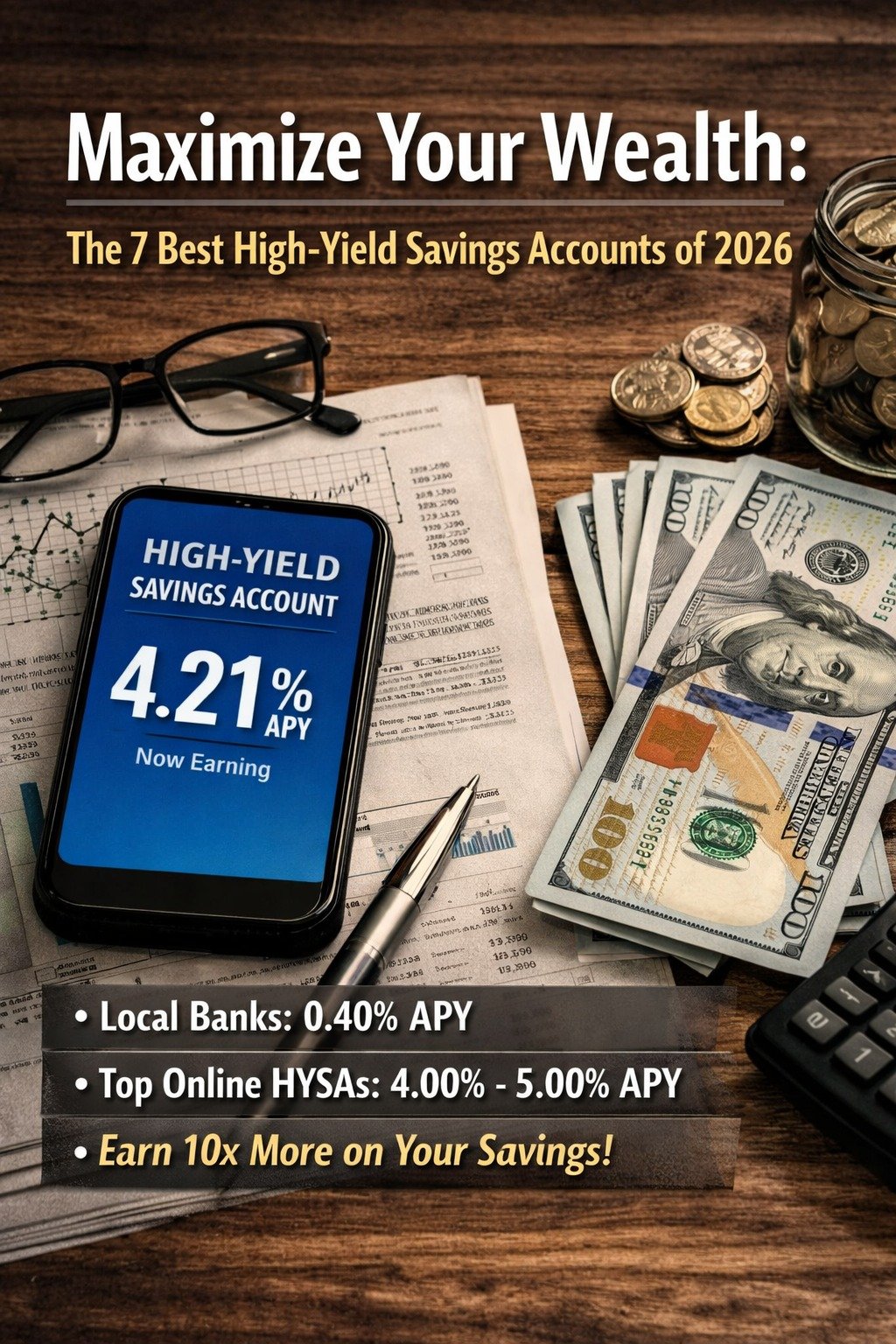

In the financial landscape of 2026, the mantra “cash is king” has taken on a new meaning. While the volatile markets of previous years have taught investors the value of diversification, the High-Yield Savings Account (HYSA) remains the cornerstone of a sophisticated financial plan. With interest rates stabilizing after the Federal Reserve’s recent adjustments, the difference between a traditional big-box bank and a top-tier online HYSA can mean thousands of dollars in “lazy money” left on the table.

Why Your Local Bank is Costing You Money

Most Americans still keep their emergency funds in “brick-and-mortar” institutions. As of March 2026, the national average savings rate sits at a meager 0.40% APY. In contrast, the leading digital-first banks are offering rates upwards of 4.21% APY.

If you have $25,000 in a traditional account, you might earn $100 in a year. In a top-tier HYSA, that same balance could generate over $1,000. This isn’t just “extra change”—it’s a powerful hedge against inflation and a critical tool for compound interest.

The Top 7 High-Yield Savings Accounts of 2026

- Axos ONE®: The Efficiency Leader

Current APY: Up to 4.21%

Best For: Savers who use direct deposit and want a unified banking experience.

Axos Bank has reclaimed its spot at the top of the leaderboard in 2026 with the Axos ONE® bundle. By combining a checking and savings experience, they offer a tiered interest rate that rewards active users. To hit the 4.21% mark, users typically need to maintain a qualifying monthly direct deposit of $1,500.

Pros: High ceiling for interest; no monthly maintenance fees.

Cons: Requires direct deposit to unlock the highest tier. - SoFi Banking: The Best Overall Ecosystem

Current APY: Up to 4.00% (with SoFi Plus)

Best For: Modern professionals and “all-in-one” seekers.

SoFi continues to dominate the “Fintech” space. In 2026, their SoFi Plus program offers a significant boost to the standard savings rate. What sets SoFi apart isn’t just the rate, but the “Vaults” feature, allowing you to organize your savings into specific goals like “Home Down Payment” or “Dream Vacation” within a single account.

Pros: No account fees; up to $2M in FDIC insurance through their partner network.

Cons: The highest rates are reserved for members with active direct deposits. - Openbank by Santander: The Global Powerhouse

Current APY: 4.09%

Best For: Security-conscious savers who want a simple, high-yield product.

Openbank, the digital arm of Santander, has made aggressive moves in the U.S. market this year. They offer a straightforward 4.09% APY with a relatively low barrier to entry. It is a “pure” savings play for those who don’t want to deal with complex requirements or multiple account tiers.

Pros: High base rate without “hoop-jumping”; backed by a global banking giant.

Cons: Customer service is primarily digital-only. - Marcus by Goldman Sachs®: The Gold Standard for Stability

Current APY: 3.65% + Referral Bonuses

Best For: Conservative investors looking for institutional reliability.

While Marcus may not always have the absolute highest “sticker price” rate, they offer a level of stability and brand trust that is hard to beat. Their app remains the most user-friendly in the industry. In 2026, Marcus frequently offers “Rate Boost” promotions for referrals, which can temporarily push your APY well above 4.50%.

Pros: No minimum deposit; seamless interface; excellent “refer-a-friend” perks.

Cons: Lower base rate than aggressive fintech competitors. - Varo Bank: The High-Yield Specialist

Current APY: Up to 5.00% (on first $5,000)

Best For: Small emergency funds and “starter” savers.

Varo remains a unique player in 2026. For balances up to $5,000, they offer a market-leading 5.00% APY, provided you meet their direct deposit and debit card usage requirements. It is arguably the best “starter” account for someone building their first emergency fund.

Pros: Highest available rate for lower balances.

Cons: Rate drops significantly on balances exceeding the $5,000 cap. - CIT Bank: The Choice for Large Balances

Current APY: 3.75% (Platinum Savings)

Best For: Those with $5,000 or more to deposit.

CIT Bank’s Platinum Savings account is designed for the serious saver. While their base rate is competitive, they reserve their best yields for customers who maintain a balance of at least $5,000. It is a no-frills, high-performance account for those who already have a solid financial foundation.

Pros: Strong history of competitive rates; reliable mobile app.

Cons: Not ideal for those with less than $5,000 in liquid savings. - American Express® National Bank: The Brand of Trust

Current APY: 3.30%

Best For: Existing Amex cardholders looking for seamless integration.

While the APY is slightly lower than the fintech “disruptors,” American Express provides an elite customer service experience and a rock-solid platform. For users who already have an Amex Gold or Platinum card, the ability to see your savings and credit card balance in one app is a major convenience factor.

Pros: World-class customer service; incredibly easy setup.

Cons: Yield is lower than online-only competitors.

🛠️ Key Factors to Consider When Choosing a Bank

FDIC Insurance: The Non-Negotiable

In 2026, online security is paramount. Never deposit money into an account that is not FDIC-insured. This guarantees your deposits up to $250,000 per depositor, per institution. Some banks, like SoFi, use a “sweep” network to provide coverage up to $2M—a crucial feature for high-net-worth individuals.

Compound Interest Frequency

The secret to wealth isn’t just the rate—it’s the frequency. Look for accounts that compound interest daily. This means you earn interest on your interest every single day, rather than just once a month. Over several years, this can add a significant “hidden” boost to your returns.

Liquidity and Access

An emergency fund is only useful if you can access it. While HYSAs are liquid, some banks have a 1–3 day lag for external transfers. If you need instant access, look for banks that offer a linked ATM card or real-time transfers to a companion checking account.

📈 2026 Market Outlook: Where are Rates Heading?

The economic consensus for the remainder of 2026 suggests a “plateau” in interest rates. While we likely won’t see the 5%+ rates of 2024 again soon, the current environment of 3.5%–4.2% is historically excellent. Financial experts recommend locking in rates now before any further potential cuts by the central bank later this year.

Conclusion: Your Next Step to Financial Freedom

Choosing the right high-yield savings account is one of the lowest-effort, highest-reward moves you can make for your personal finance journey. By moving your money to one of the top 7 providers listed above, you are essentially giving yourself a “passive raise” without any additional work.

Action Item: Review your current savings rate today. If it’s below 3%, choose one of the top 3 banks on this list and start your application. Most take less than 10 minutes to complete.

Author

queenalisha232@gmail.com

Related Posts

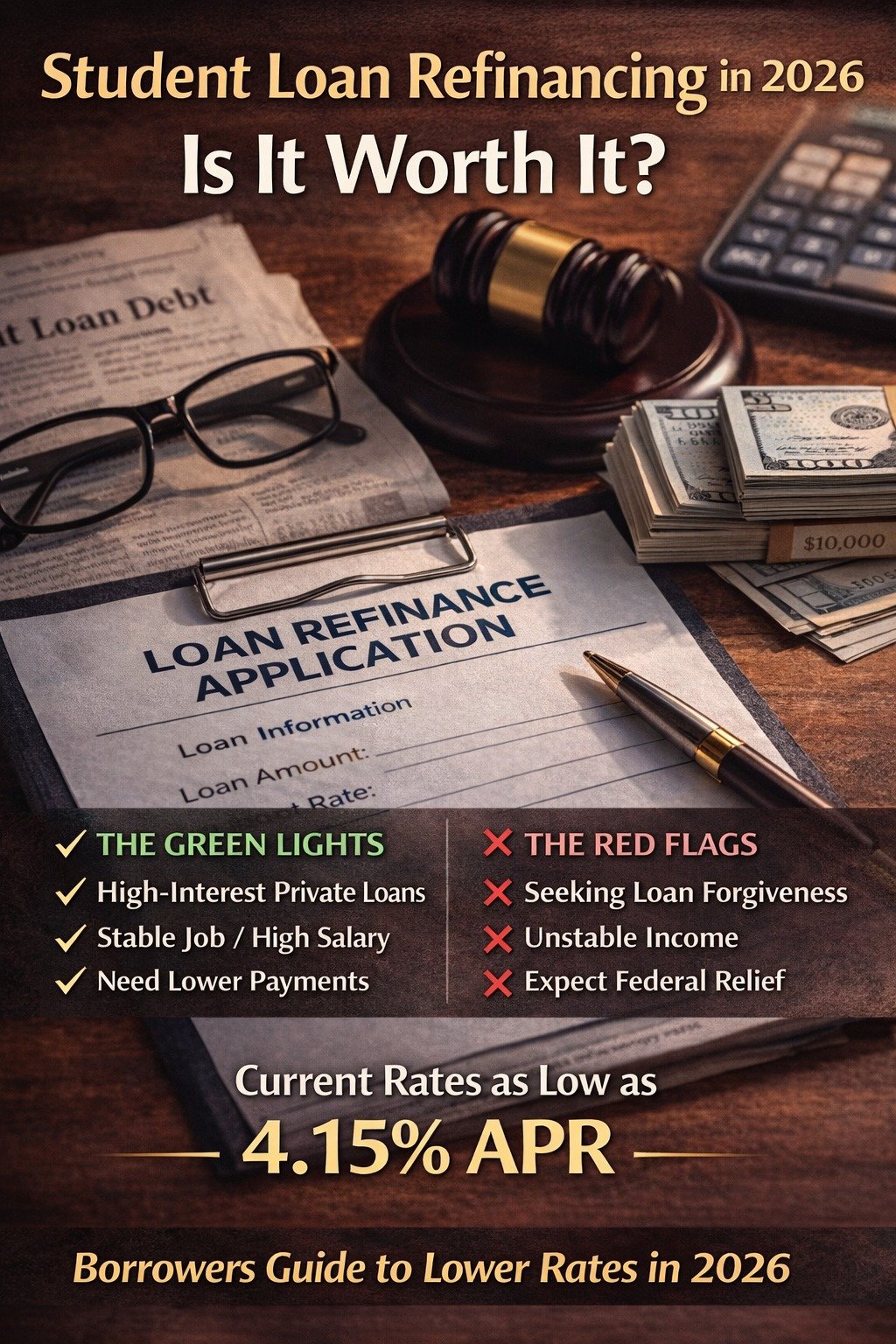

Student Loan Refinancing in 2026: Is It Worth It?

For years, student loan borrowers were told to “wait and see” as federal payment pauses and forgiveness debates dominated the headlines. However,...

Read out all

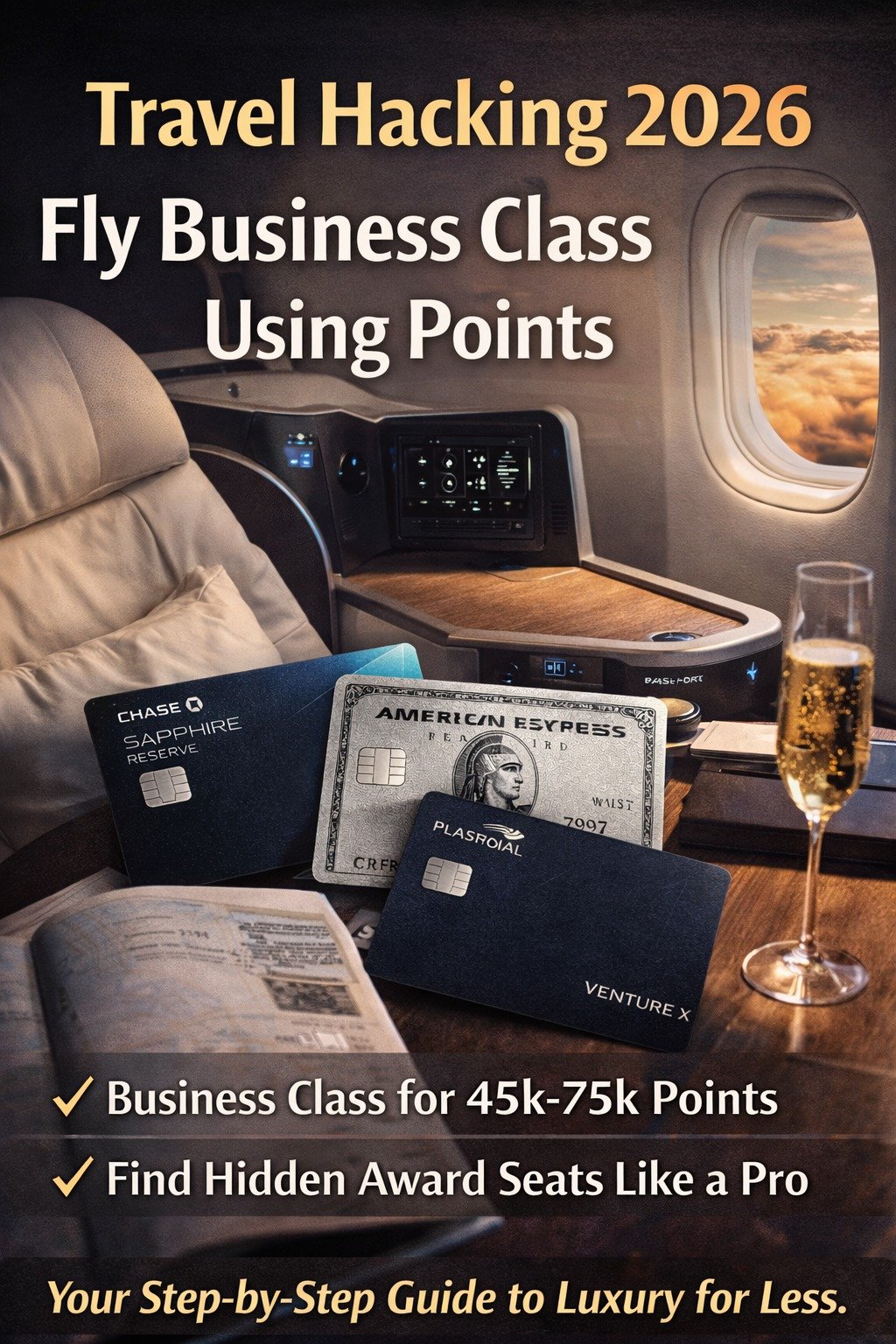

Travel Hacking 2026: How to Fly Business Class Using Credit Card Points

In the golden age of travel hacking, flying Business Class is no longer a luxury reserved for the 1%. In 2026, it...

Read out all

The 800 Club: How to Build a Perfect Credit Score in 12 Months (2026 Guide)

The 800 Club: How to Build a Perfect Credit Score in 12 Months (2026 Guide)In the financial landscape of 2026, an 800...

Read out all

The Ultimate Guide to Choosing Your First Premium Credit Card (2026 Edition)

In the modern financial ecosystem, a credit card is no longer just a plastic tool for debt—it is a high-performance financial instrument....

Read out all