For years, student loan borrowers were told to “wait and see” as federal payment pauses and forgiveness debates dominated the headlines. However, as of March 2026, the dust has settled. We now have a clear view of the new Repayment Assistance Plan (RAP) and the stabilized private lending market.

Refinancing—the process of taking out a new loan with a private lender to pay off your old ones—can be a powerful tool to lower your interest rate or monthly payment. But in 2026, the stakes are higher because once you leave the federal system, there is no going back.

🏛️ The “OBBBA” Factor: What Changed on July 1, 2026?

The One Big Beautiful Bill Act (OBBBA) has fundamentally restructured federal student aid. If you are considering refinancing federal loans into private ones, you must understand what you are giving up:

Elimination of Grad PLUS: For new borrowers starting after July 2026, Graduate PLUS loans have been eliminated. If you currently hold these, they are a “legacy” asset with unique protections.

The RAP Plan: The newly created Repayment Assistance Plan (RAP) has replaced older Income-Driven Repayment (IDR) plans. It offers a streamlined path to forgiveness and caps payments more aggressively than previous models.

New Loan Limits: With federal borrowing now capped at $20,500/year for most graduate programs, the private market has become more competitive, leading to better “Refi” offers for high-income earners.

📈 The Interest Rate Environment of 2026

As of Q1 2026, the Federal Reserve has successfully “landed the plane” on inflation, leading to a stabilization of benchmark rates.

Federal Rates (2025-2026): Current undergraduate rates sit at 6.39%, while Graduate Unsubsidized loans are at 7.94%. Parent and Grad PLUS loans are at a steep 8.94%.

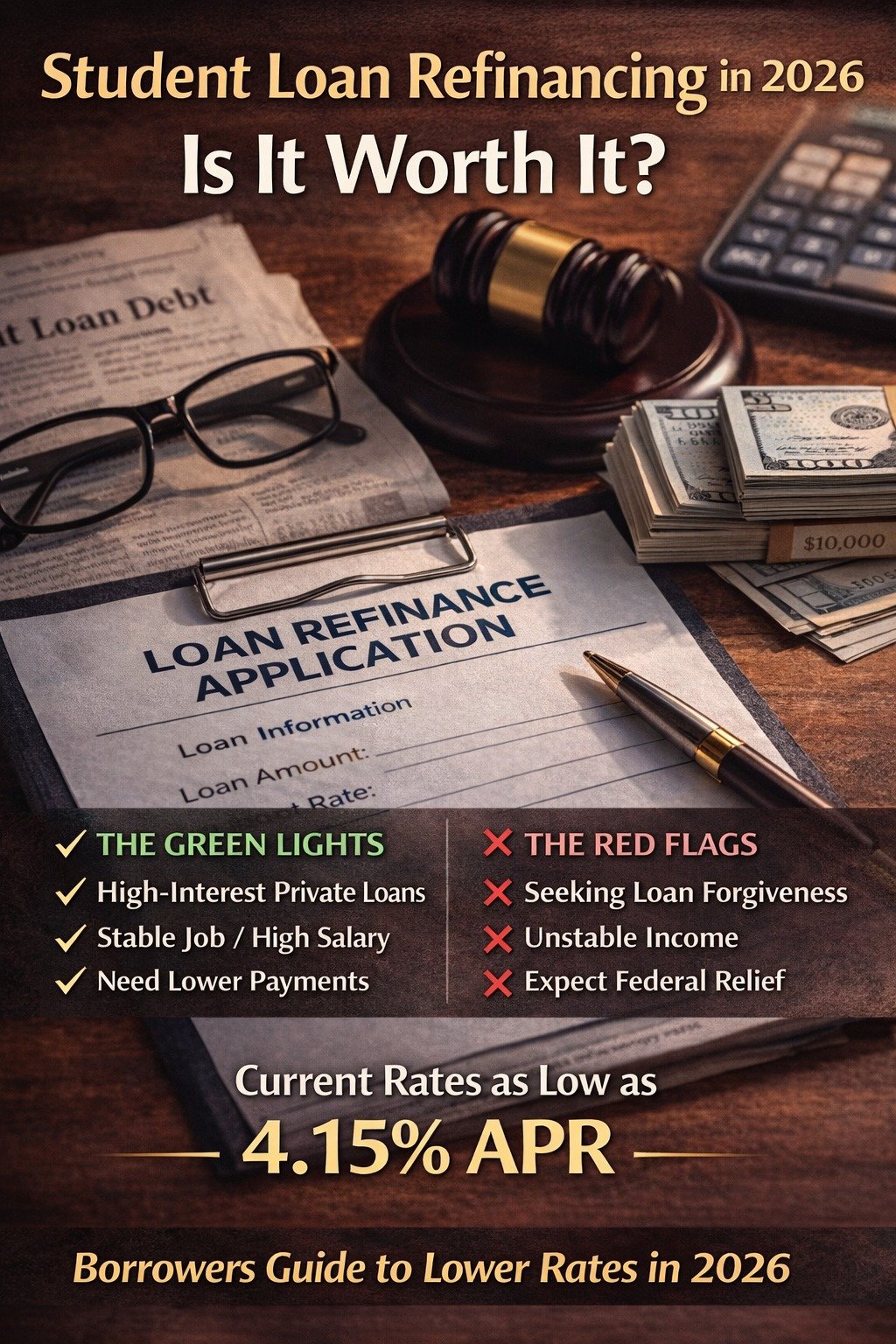

Private Refinance Rates: For borrowers with a credit score of 740+, private lenders like SoFi, Earnest, and Laurel Road are offering fixed rates as low as 4.15% to 5.25%.

The Math: If you are sitting on $100,000 in legacy federal loans at 8%, and you qualify for a private refi at 4.5%, you are looking at nearly $200 a month in pure interest savings. Over a 10-year term, that is $24,000 back in your pocket.

✅ When Refinancing is “Worth It” (The Green Lights)

- You Have High-Interest Private Loans

This is a “no-brainer.” If you already have private student loans (Sallie Mae, etc.) at 10% or 12%, you should refinance immediately. You aren’t losing any federal protections because you never had them. In 2026, the “Refi-on-Refi” trend is popular—even if you refinanced in 2024, today’s rates might be 1% lower. - You Are a “High-Earner, Not-Rich-Yet” (HENRY)

If you are a doctor, lawyer, or engineer making $150k+ and your debt-to-income ratio is healthy, you likely won’t benefit from federal “Income-Driven” plans. In this case, the lower interest rate of a private loan is your primary goal. - You Want a Single, Simpler Payment

Managing seven different federal “sub-loans” with different servicers is a headache. Refinancing collapses these into one monthly bill with one digital dashboard.

❌ When to Avoid Refinancing (The Red Flags) - You Are Pursuing Public Service Loan Forgiveness (PSLF)

If you work for a non-profit or the government, do not refinance federal loans. The moment you move to a private lender, you are disqualified from PSLF. In 2026, PSLF processing has become much faster, making it more valuable than ever to stay in the federal system. - You Have Unstable Income

Federal loans offer Deferment and Forbearance if you lose your job. Private lenders in 2026 have improved their “hardship” programs, but they are not as robust as the federal government’s legal requirements. - You Expect to Use the RAP Plan

If your income is low relative to your debt, the RAP plan’s $0 or capped payments may actually save you more money over time than a lower interest rate would.

🛠️ The 2026 Refinancing Checklist

Before you sign a new loan agreement, ensure you’ve checked these four boxes:

Credit Score Audit: You need a 670 minimum, but 740+ is where the “High-CPM” rates live.

Debt-to-Income (DTI) Check: Most 2026 lenders want to see that your total monthly debt payments (including the new loan) are under 40% of your gross monthly income.

The “Fixed vs. Variable” Decision: While variable rates are tempting at 3.8%, the 2026 forecast suggests a slight upward tick toward 2027. Fixed rates are the safer bet for long-term peace of mind.

Co-signer Release: If you use a co-signer to get a better rate, ensure the contract has a “release” clause that triggers after 12–24 months of on-time payments.

💡 Summary: The Verdict for 2026

Is student loan refinancing worth it this year? Yes, if you have private loans or high-interest federal loans and don’t qualify for forgiveness. The 2.5% to 3% interest gap between 2026 private rates and federal PLUS rates is too large to ignore for those with stable careers. However, with the OBBBA reforms now in effect, the “insurance” of federal protections has a higher “value” than it did two years ago. Calculate your “Protection Premium” before making the leap.

Author

queenalisha232@gmail.com

Related Posts

Travel Hacking 2026: How to Fly Business Class Using Credit Card Points

In the golden age of travel hacking, flying Business Class is no longer a luxury reserved for the 1%. In 2026, it...

Read out all

The 800 Club: How to Build a Perfect Credit Score in 12 Months (2026 Guide)

The 800 Club: How to Build a Perfect Credit Score in 12 Months (2026 Guide)In the financial landscape of 2026, an 800...

Read out all

The Ultimate Guide to Choosing Your First Premium Credit Card (2026 Edition)

In the modern financial ecosystem, a credit card is no longer just a plastic tool for debt—it is a high-performance financial instrument....

Read out all

Maximize Your Wealth: The 7 Best High-Yield Savings Accounts of 2026

In the financial landscape of 2026, the mantra “cash is king” has taken on a new meaning. While the volatile markets of...

Read out all